Fighting in the Persian Gulf has caused oil prices to jump sharply. Many analysts now think the Consumer Price Index (CPI) will rise faster. Because oil is used in many products, a higher CPI seems likely. The big question is how high CPI can go before it hurts the stock market’s upward trend.

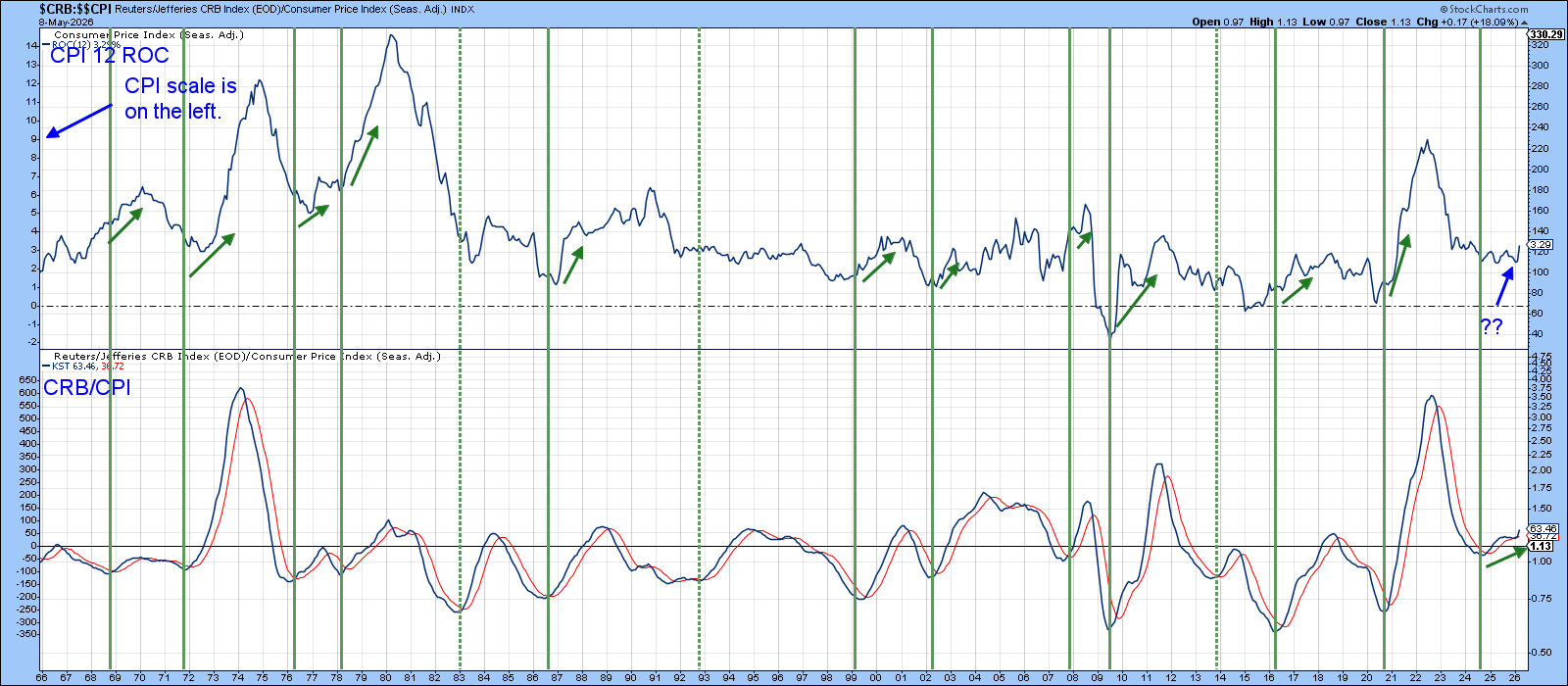

Before answering that, it helps to see how commodity prices affect the CPI. Commodity prices sit at the start of the production chain, so they are often the first sign of rising consumer prices.

Chart 1 compares the year‑over‑year change in CPI with a long‑term indicator that measures the CRB Composite relative to CPI. The low points on the indicator usually appear before the CPI starts to rise. This shows that commodity momentum often precedes consumer inflation by a few months. The chart does not tell us how big the CPI rise will be, only that the odds are higher when commodity momentum turns up.

Chart 2 looks at the CPI alongside the S&P Composite that has been adjusted for inflation. A red line at 5 % marks a level where stocks have historically become vulnerable. Whenever an 18‑month rate‑of‑change line crosses above 5 %, equity prices tend to fall. Falling back below 5 % does not always end a bear market, and a prolonged reading above 5 % does not always mean disaster, but the risk is clear.

Today the CPI is just under the 5 % line, leaving little room for error. The recent surge in commodity prices suggests more upward pressure is moving through the early stages of the inflation pipeline. A small extra rise could push the 18‑month rate‑of‑change above the warning level and trigger a formal alert.

Even if the conflict eases and oil prices drop, the economy will still face underlying inflation pressures that can push the CPI higher. In either case, stocks that are adjusted for inflation are likely to feel the strain.

Good luck and happy charting.

Source: Materials provided by https://articles.stockcharts.com.Note: Content may be edited for style and length.