Navigating Volatility with a Defensive Portfolio

The S&P 500 jumped almost 3.5% last week, but the list of its top five sectors stayed the same. Even though world events are making markets shaky, the rankings haven’t moved. Because the rankings are steady, the plan is to stay out of the current turbulence and keep the same sector mix.

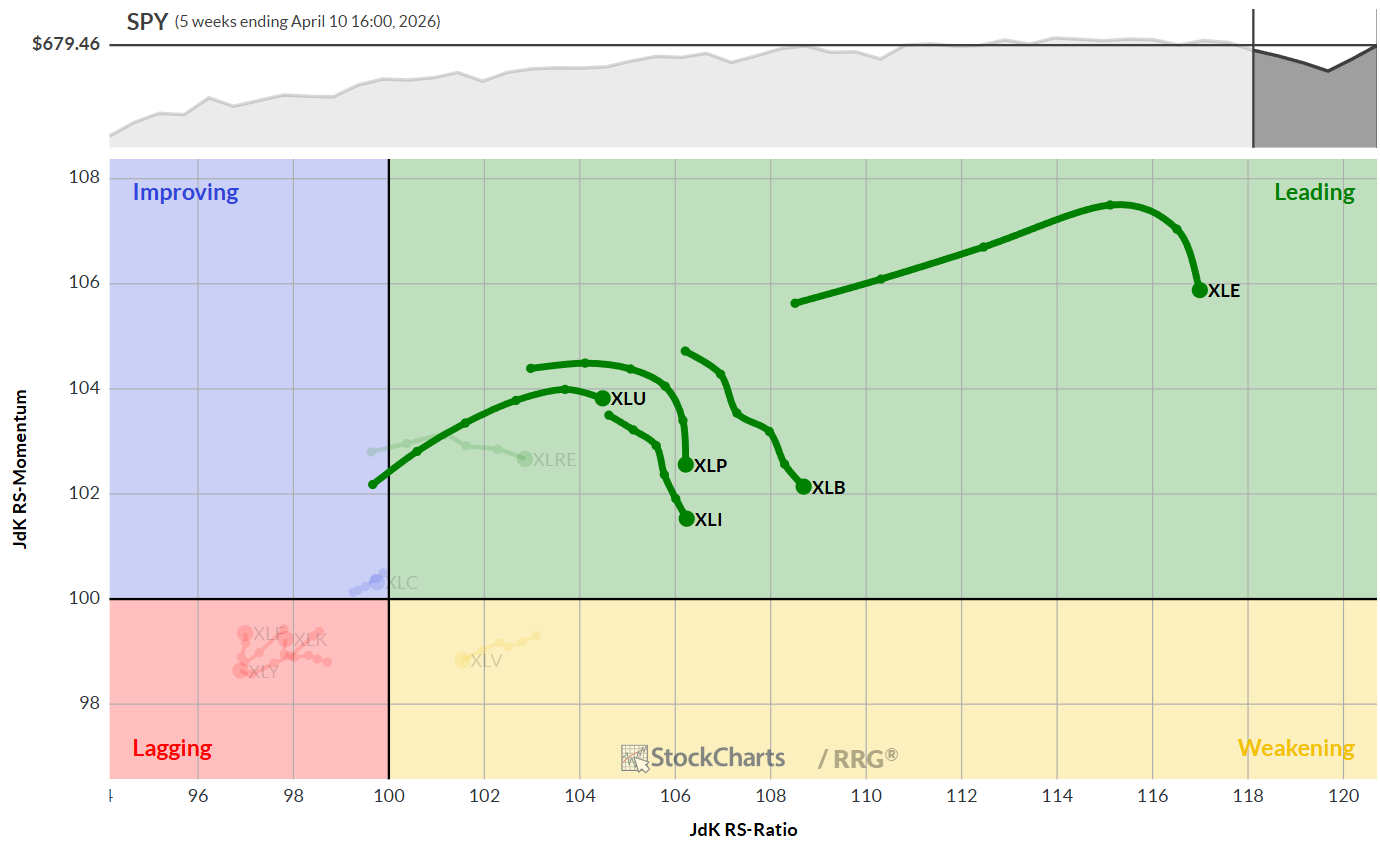

At the end of the week the Energy sector led the pack, followed by Materials, Industrials, Consumer Staples and Utilities. In the lower half, Real Estate moved up a spot, while Health Care slipped down. The bottom of the list still holds Communication Services, Technology, Financials and Consumer Discretionary.

- Energy – XLE (15%)

- Materials – XLB (10%)

- Industrials – XLI (40%)

- Consumer Staples – XLP (25%)

- Utilities – XLU (10%)

- Real Estate – XLRE*

- Health Care – XLV*

- Communication Services – XLC

- Technology – XLK

- Financials – XLF

- Consumer Discretionary – XLY

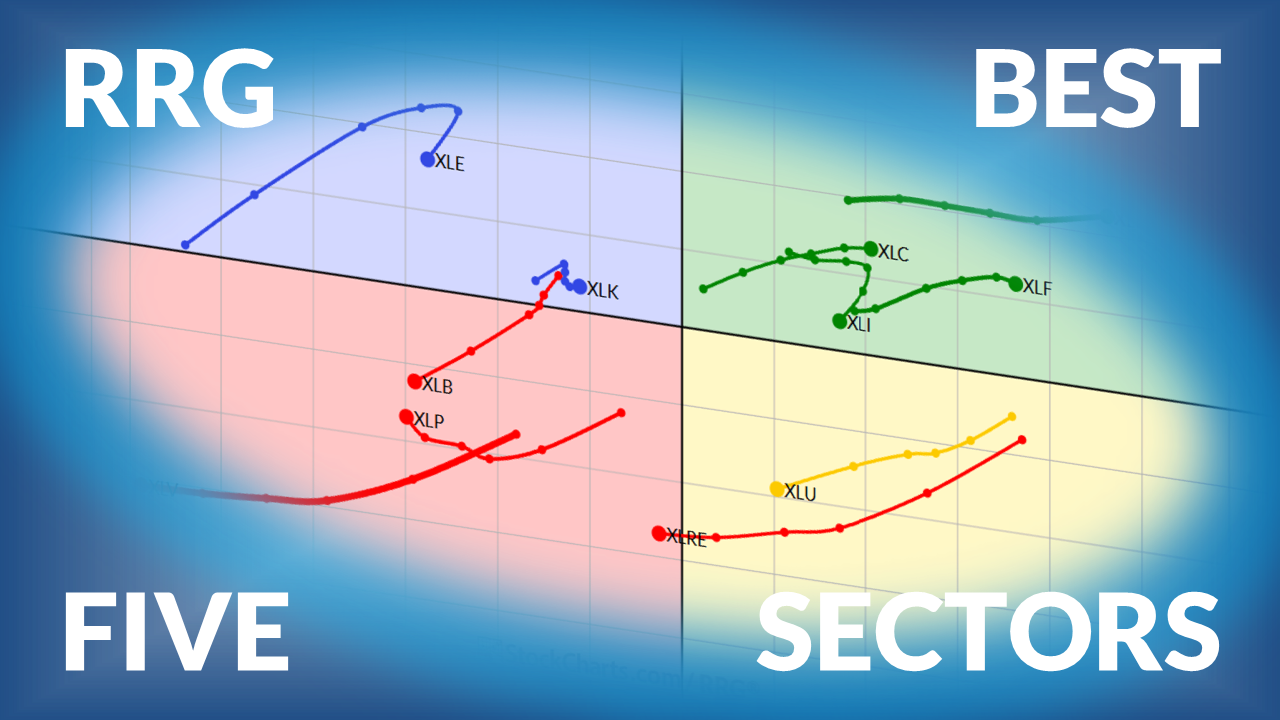

Weekly Relative Rotation Graph

All five leading sectors stay in the “leading” quadrant of the weekly RRG. They keep climbing the RS‑ratio line, but a little momentum is slipping. This means the weekly up‑trend is still there, even if it feels a bit weaker for now.

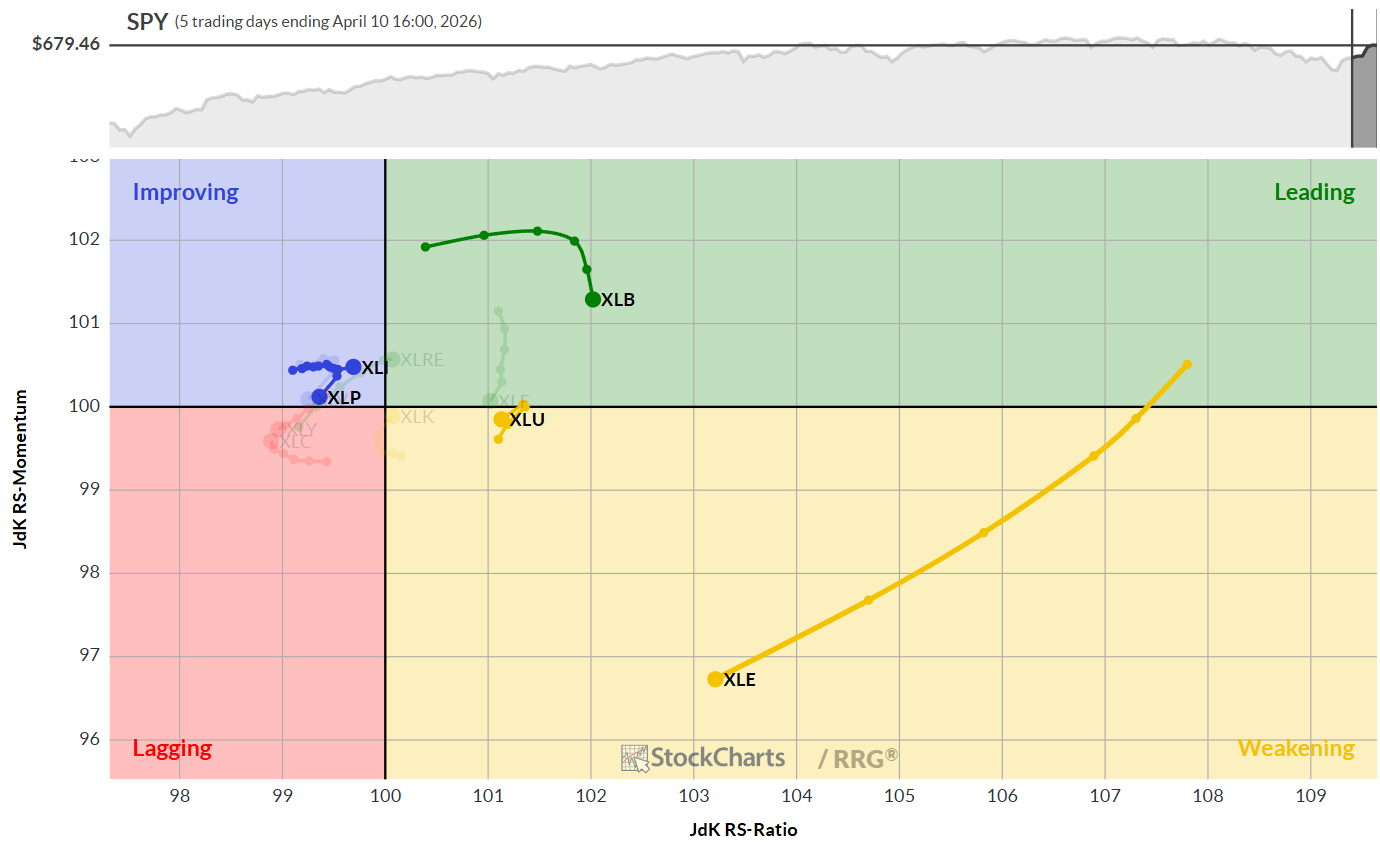

Daily Relative Rotation Graph

The daily chart shows a mixed picture:

- Materials: Still in the leading quadrant but starting to lose a bit of steam.

- Energy: Dropped deep into the weakening quadrant, losing momentum quickly after a strong week.

- Utilities: Made a short turn toward the leading area, then hooked back left, indicating a stable upward trend.

- Industrials & Consumer Staples: Both sit in the improving quadrant, close to the S&P 500’s center line. Industrials are almost back in the leading zone, while Consumer Staples are drifting toward lagging.

Sector Highlights

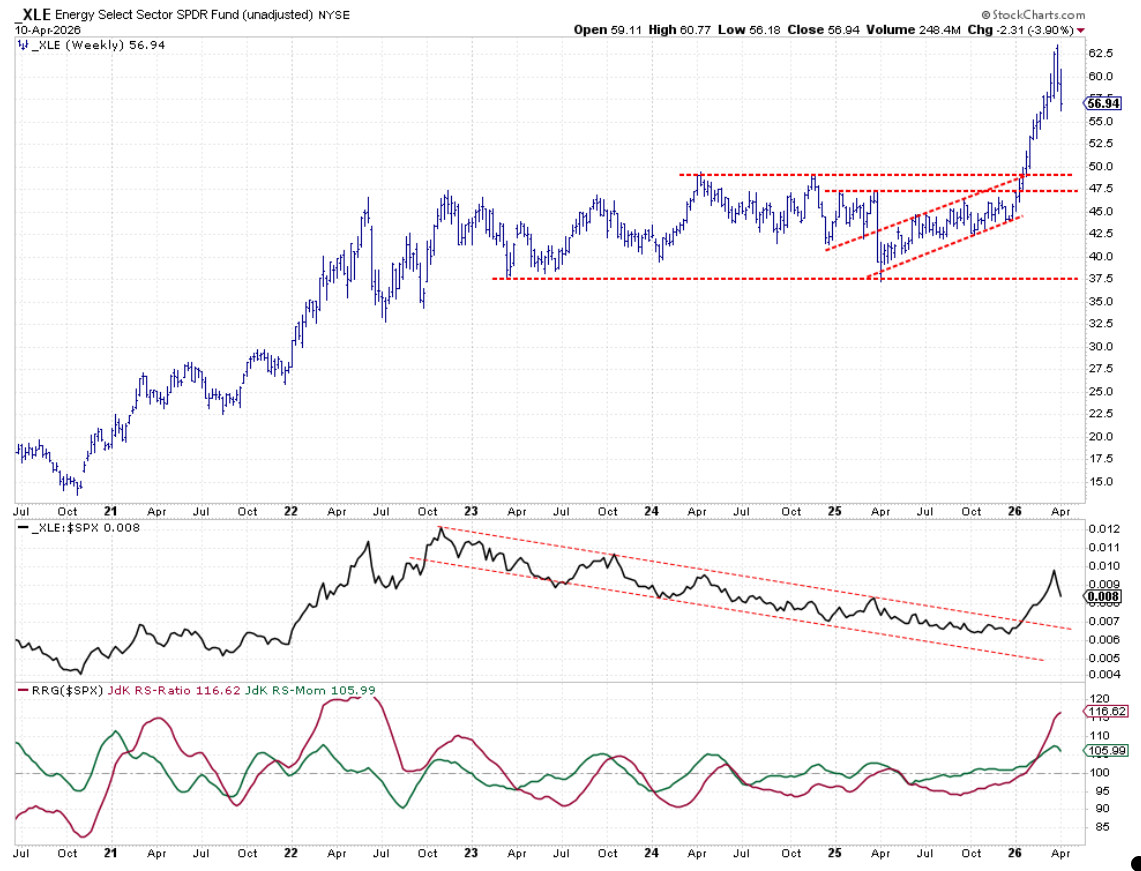

Energy

Energy broke out just under $50, climbed to about $62.50 and is now taking its first dip after the breakout. The next higher low will tell if the sector still has strength. The RS line also shows its first dip, but the RS‑ratio stays high.

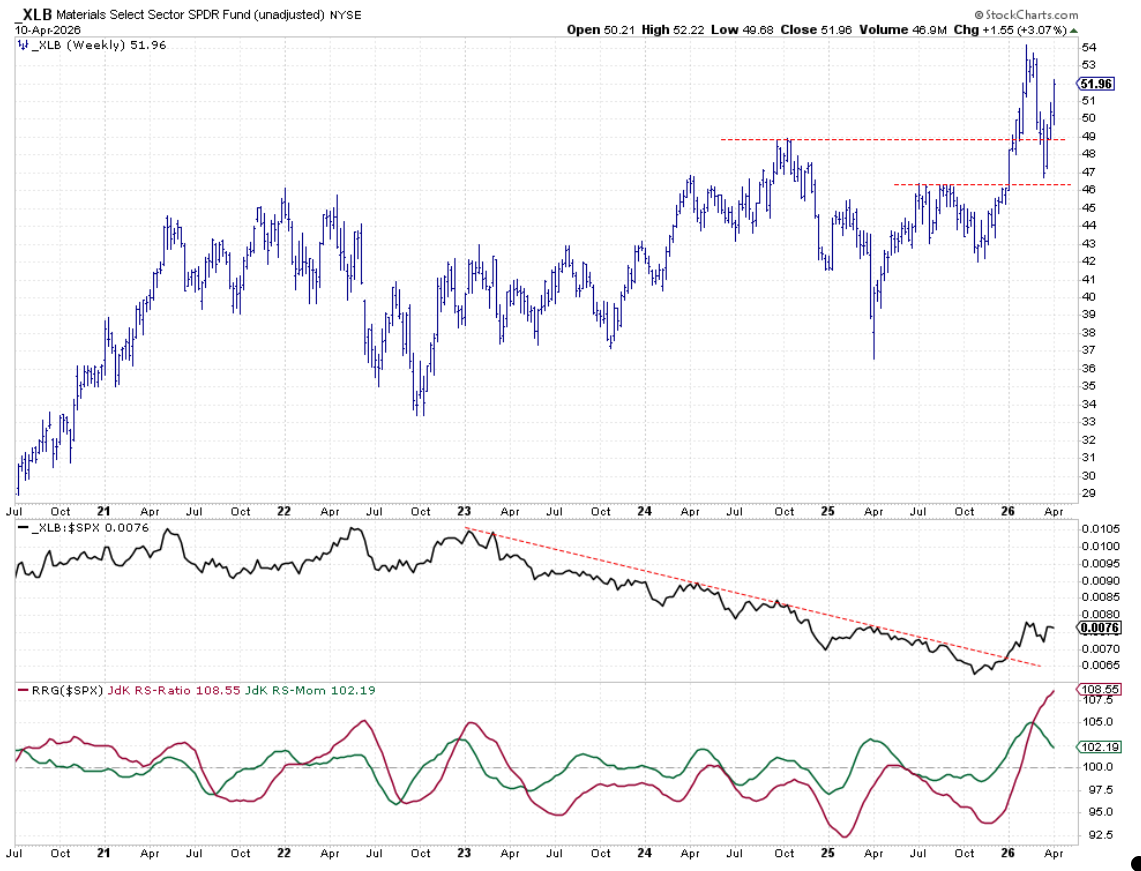

Materials

Materials set a higher low above $46, turning a former resistance into support, and are climbing back toward the all‑time high near $54. The RS line also made a higher low. A break above the previous peak would confirm strong relative strength.

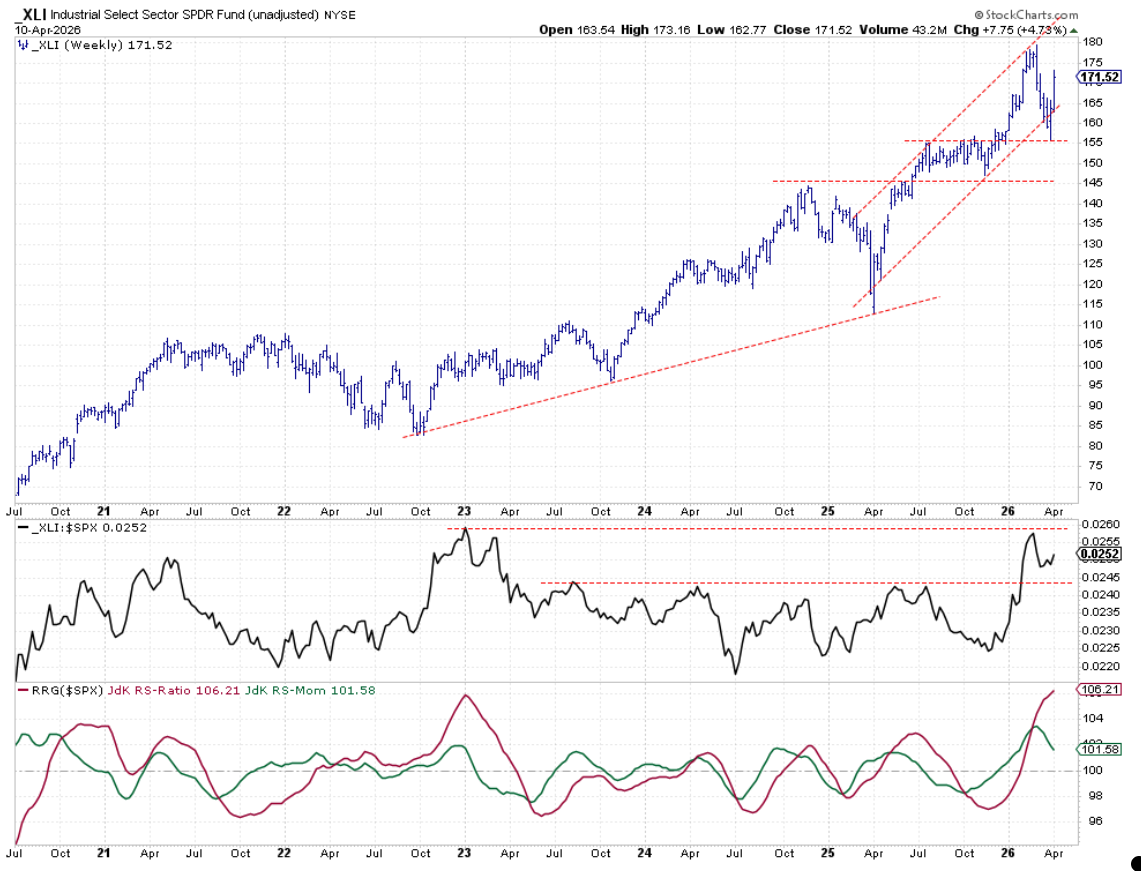

Industrials

Industrials briefly left their rising channel but are now back inside it, making a higher low around $155. The RS line hit a peak from early 2023, fell, and now shows a new higher low. Breaking the current resistance could spark a stronger rally.

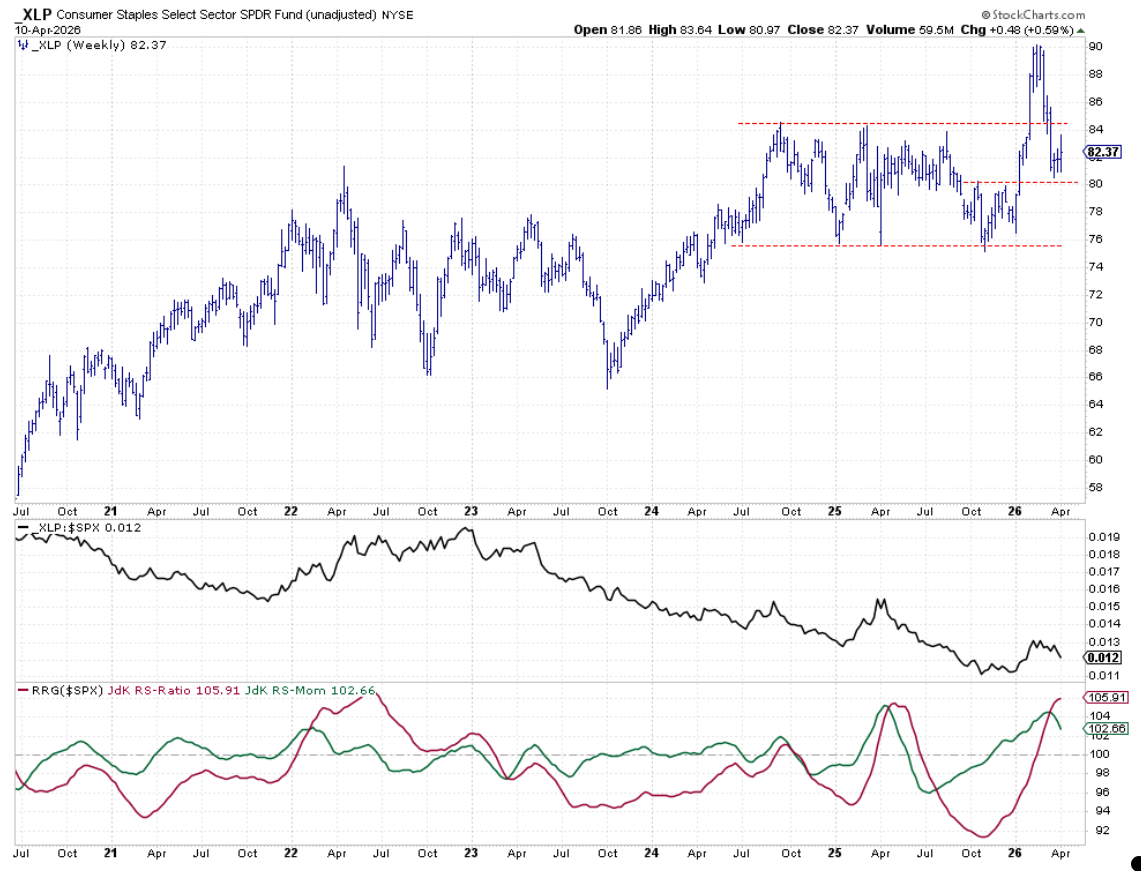

Consumer Staples

Staples fell below support, then made a higher low just above $80, turning a past resistance into support. The sector is moving back toward $84; a break above could aim for the all‑time high near $90. However, the RS line set a lower high, putting pressure on performance.

Utilities

Utilities stay strong inside a rising channel, with the price testing earlier peaks. A breakout could unlock more upside. The RS line meets resistance from last year’s highs, but both RRG lines stay well above 100, keeping Utilities in the leading quadrant.

Portfolio Perspective

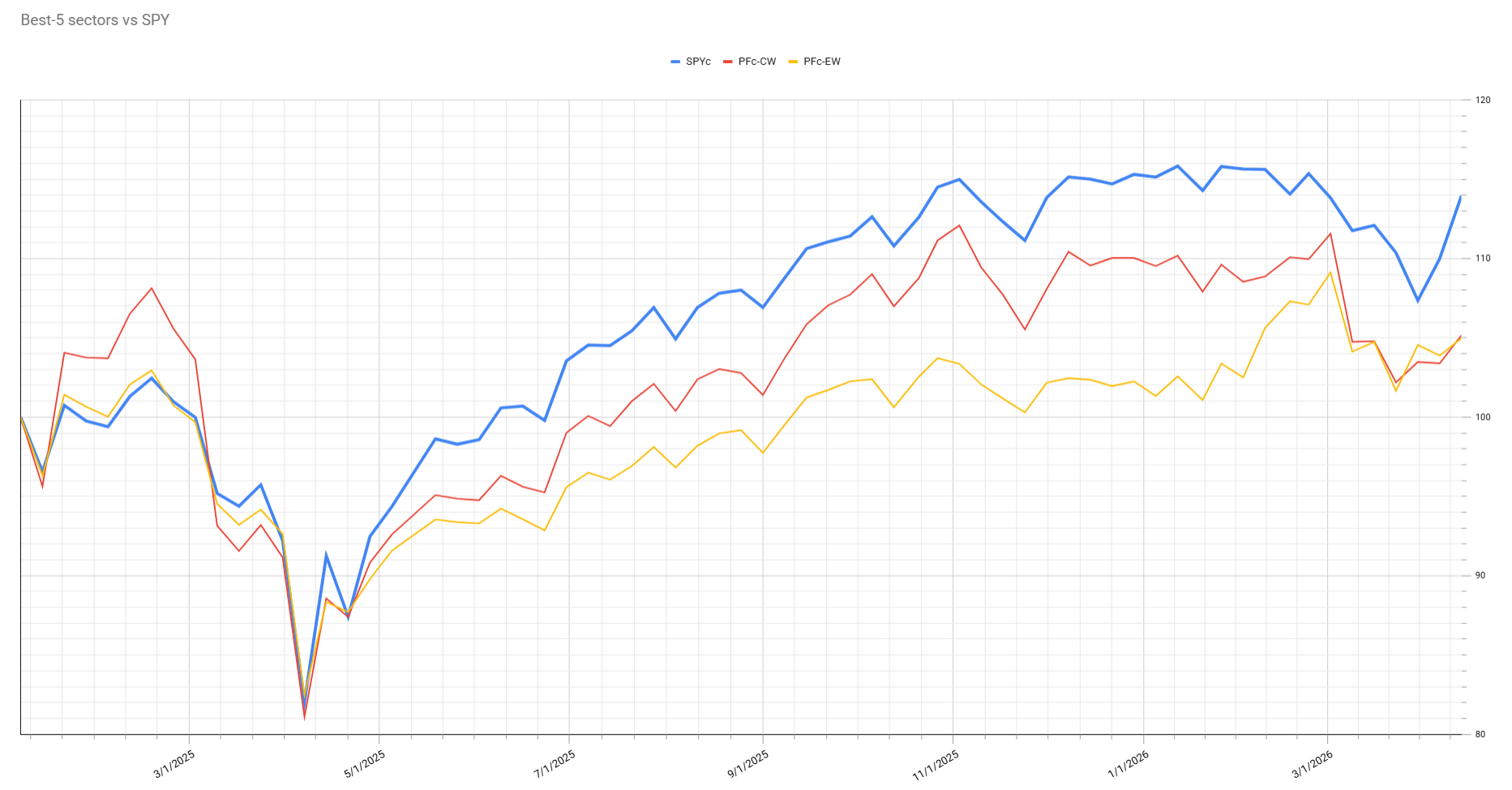

The portfolio stayed defensive last week, with Energy, Consumer Staples and Utilities making up the top holdings. As the S&P 500 surged, this defensive tilt caused the portfolio to lag about 7‑8% behind the index, erasing roughly five percentage points of relative gain over the past few weeks.

Even with the lag, the sector rankings still point to a defensive stance. Ongoing geopolitical uncertainty means market moves remain hard to predict, so staying alert is essential.

Source: Materials provided by https://articles.stockcharts.com.Note: Content may be edited for style and length.