Why Oil Prices May Keep Rising After Hormuz Tension

Many think the recent jump in oil prices will fall once ships can move freely through the Strait of Hormuz. The market feels a lot of emotion, so hopes and fears often take over. I tried to let the price itself tell the story.

When we examine the longer‑term charts, the data suggest that crude oil is on a firmer footing than most people believe. Any short‑term pullback caused by news events would likely happen inside a bigger, primary bull market. The idea is that before the Iran‑related conflict, the energy market was already ready for a major uptrend; the war simply added extra bullish icing to an already baking cake.

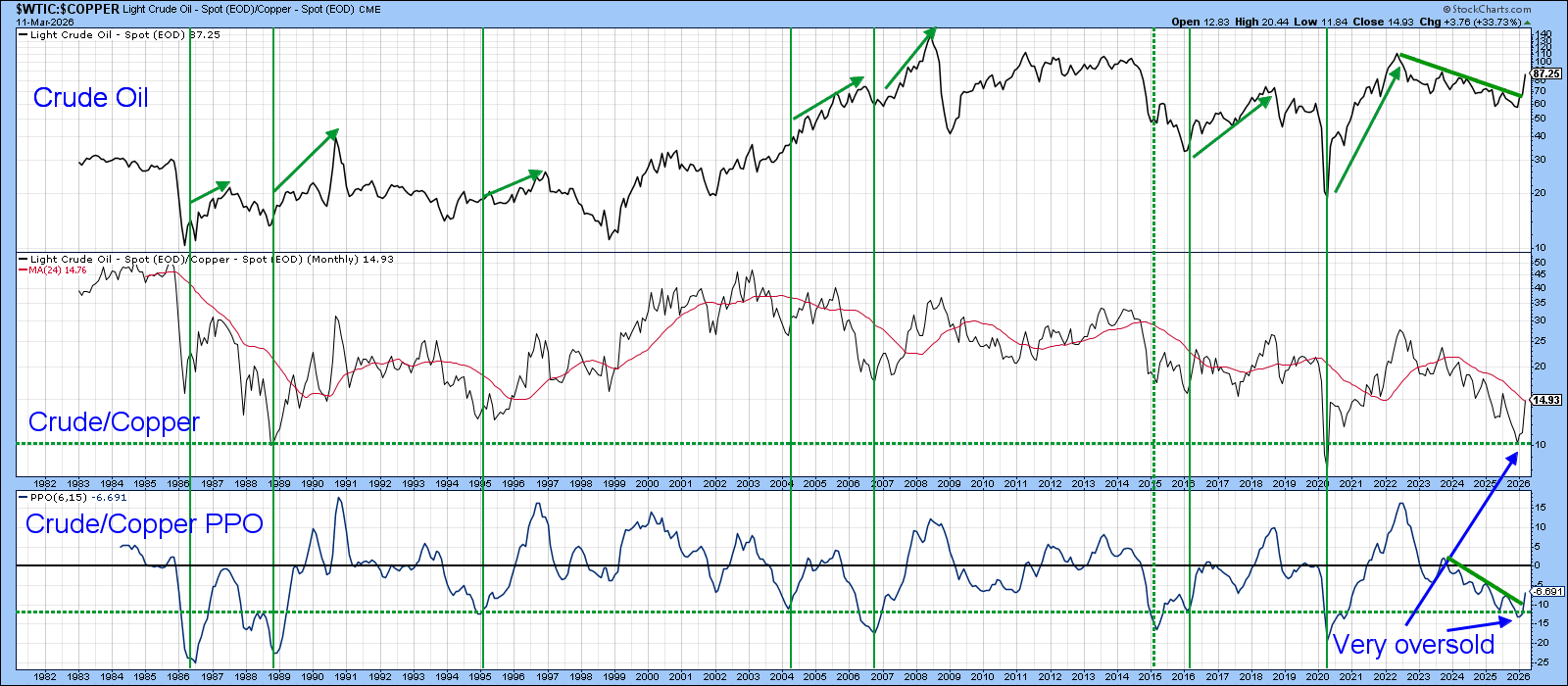

Commodity prices usually follow a repeating business‑cycle pattern. In a typical cycle, gold reaches its bottom first, then copper, and oil comes last. The chart below shows this sequence with green arrows pointing upward.

Gold moves early because it reacts to changes in inflation expectations, which happen before factories start humming again. Copper follows because it is tied directly to early‑cycle restocking of construction materials and electrical goods. Oil lags behind both because its biggest users—transport, travel, chemicals, and everyday consumer activity—grow later in the cycle.

In the current cycle, gold’s bottom appeared in 2023, copper’s in 2024, and oil did not finish its turn until early 2026. The gap between copper and oil this time is especially wide, as shown by the steep arrow linking their lows.

Momentum indicators help us see the order of these turns, but they cannot be traded directly. That’s why the next chart looks at the price relationship between copper and oil. The lower pane displays the Percentage Price Oscillator (PPO) of the copper‑to‑oil ratio using 6‑ and 15‑day settings. The vertical lines mark moments when the market was oversold and then flipped upward—signals that have often preceded year‑long oil rallies.

The March bounce, together with a clear break in the PPO trendline, points to higher oil prices—provided we get month‑end confirmation at the end of March.

U.S. economic health also matters. The chart below shows that a bull market in crude usually follows a bottom in U.S. industrial‑production momentum. The two red arrows highlight rare exceptions. The latest data suggest industrial production may have turned, which supports the case for rising oil.

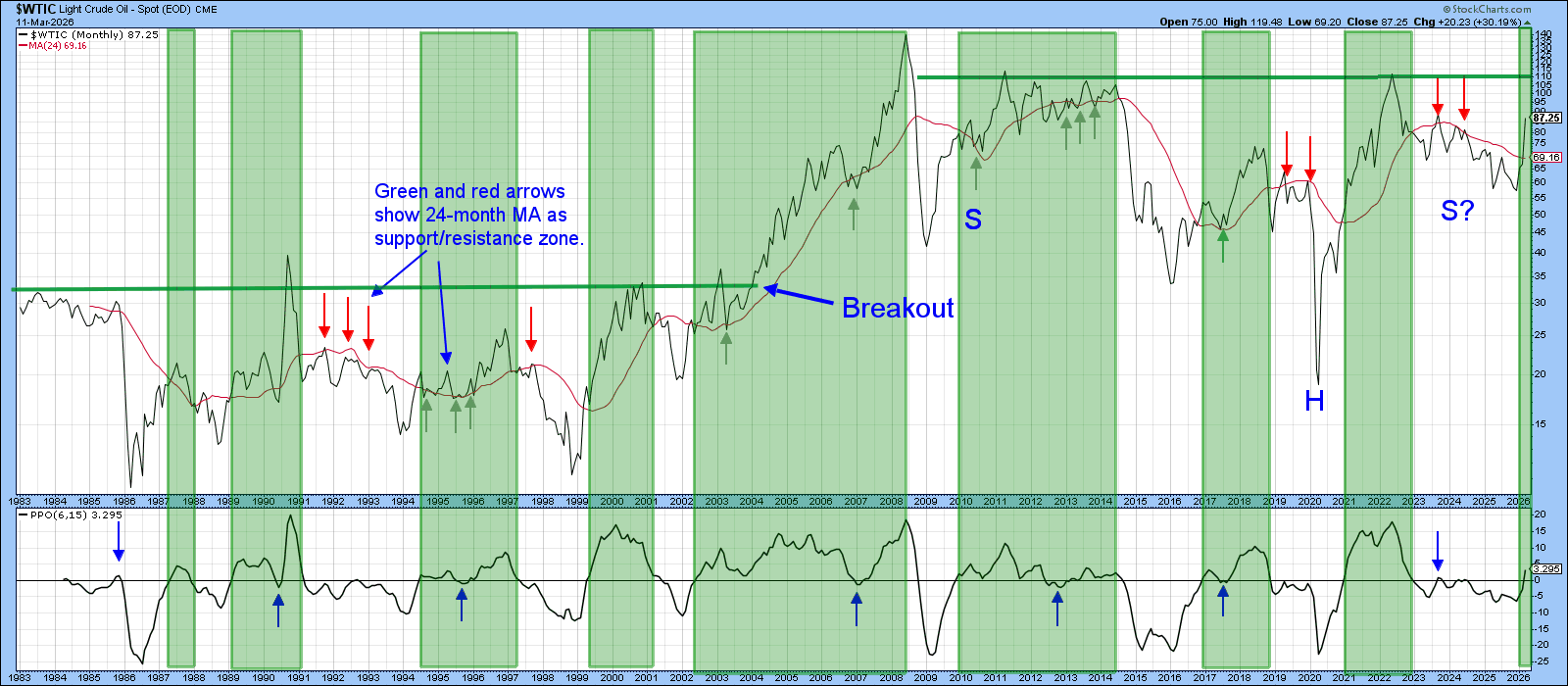

When the PPO in the lower window stays above zero, crude oil is typically in a primary bull market. The only outlier was in 1987. With month‑end data, the newest plot now gives another buy signal.

It is also possible that oil is finishing a long‑term inverse head‑and‑shoulders pattern. The potential neckline sits just above $110. A clear break above that level would echo the breakout that started the 2004 uptrend.

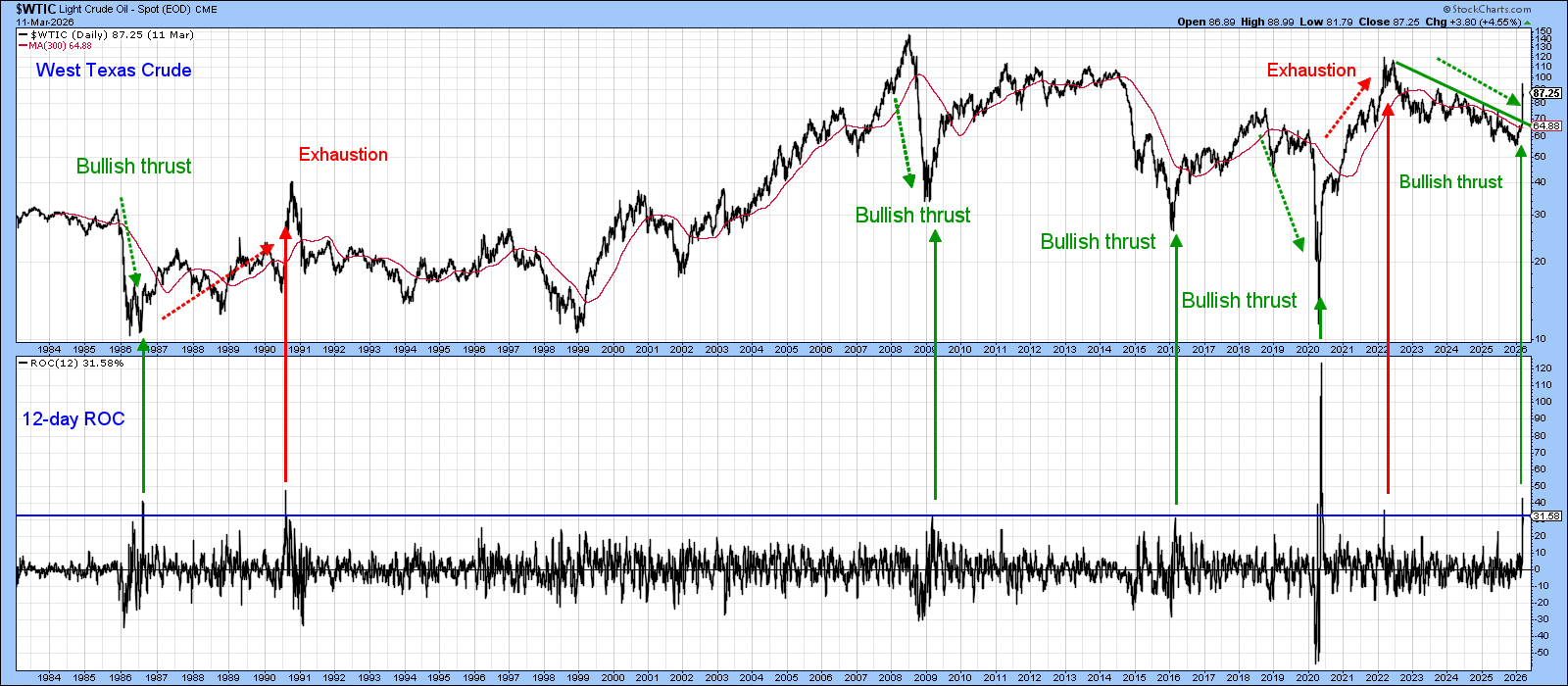

The final chart compares oil’s price to its 12‑day Rate of Change (ROC). Red and green arrows mark points where ROC peaked above the overbought line. When such a peak follows a prior bull market, it usually signals that buyers are tiring and the market may turn down. When it follows a bear market, it often marks the start of a strong new uptrend. All four past examples of the latter have led to much higher oil prices, and there is no reason to expect the current signal to behave differently.

Even if the overall direction stays up, short‑term swings are normal, especially when news events stir the market. Keep an eye on the charts, stay disciplined, and happy trading.

Source: Materials provided by https://articles.stockcharts.com.Note: Content may be edited for style and length.