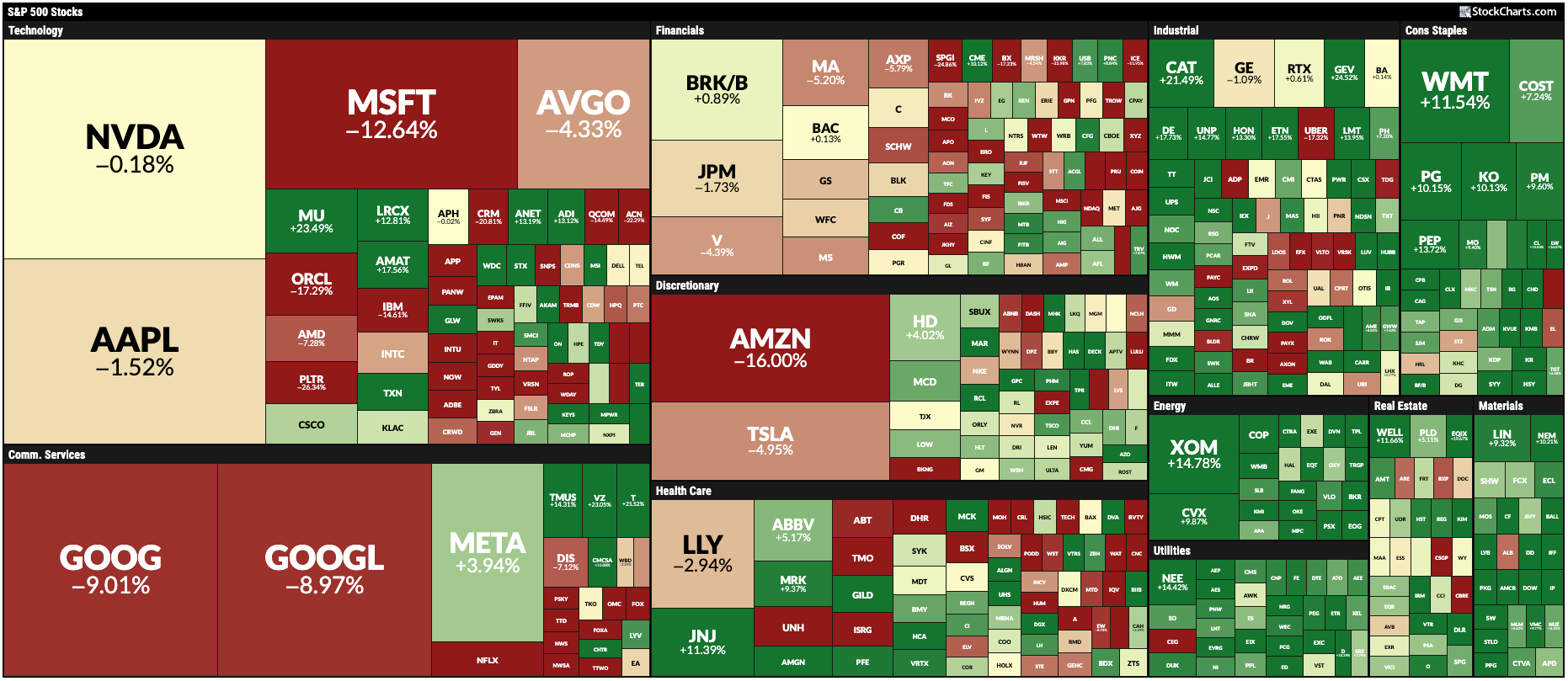

The S&P 500 market profile remains technically balanced, but a renewed Hindenburg Omen has injected a note of caution. Over the past weeks, growth‑focused equities have stumbled, allowing capital to drift into defensive arenas such as utilities, consumer staples and real estate.

Our daily market recap has highlighted a clear leadership change: cyclical groups like Industrials and Energy posted solid gains, yet it is the traditionally safe‑haven sectors that have delivered double‑digit weekly returns. This shift suggests investors are seeking stability as the year’s first quarter unfolds.

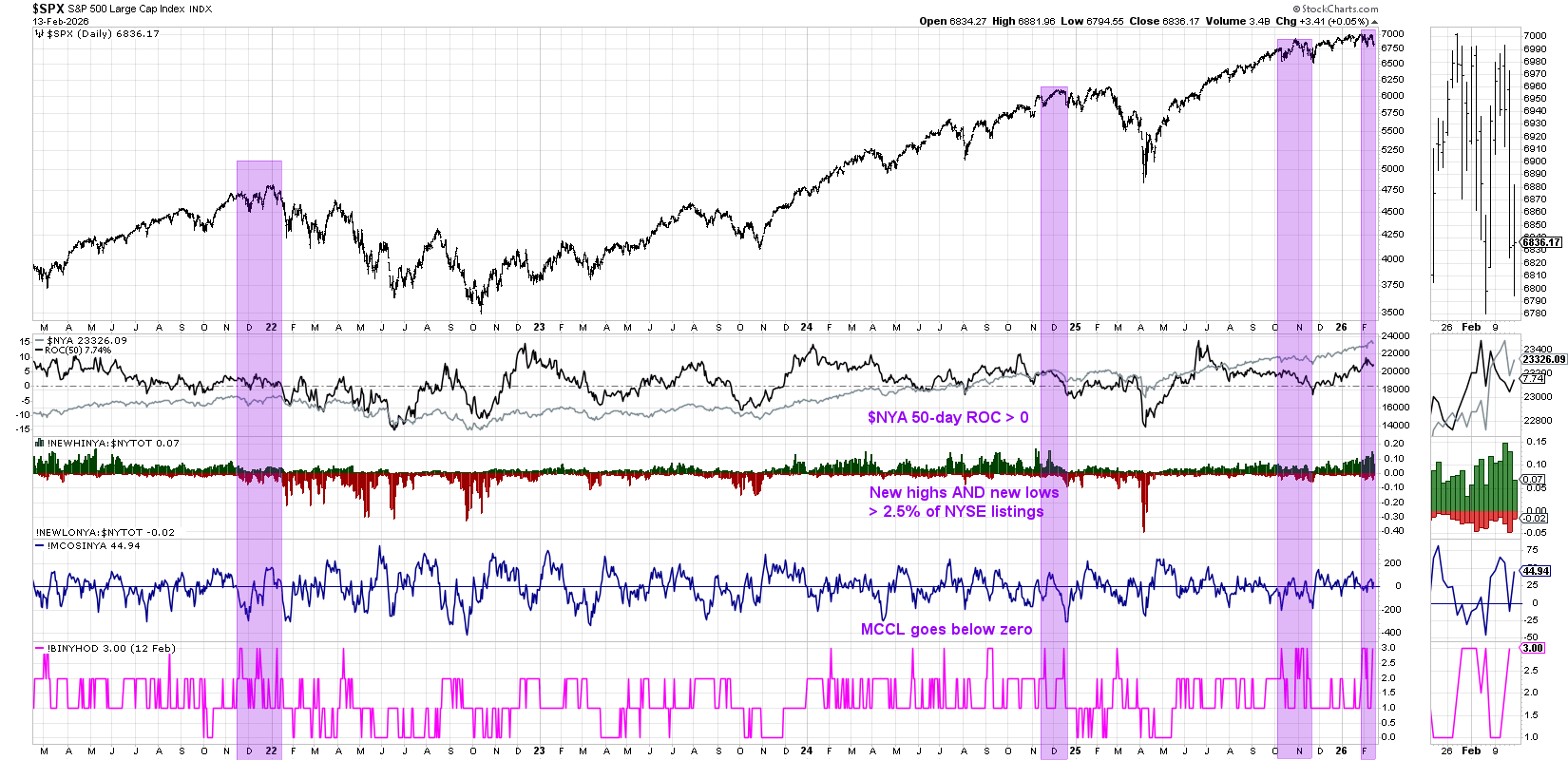

Hindenburg Omen Fires Confirmed Signal

Although mega‑cap growth names have underperformed, overall market breadth stays robust. New 52‑week highs continue to appear, just not within the lofty growth ranks. Simultaneously, enough new 52‑week lows have emerged to satisfy the criteria for the dreaded Hindenburg Omen, marking its second validated signal since the April 2025 trough.

Short‑term breadth metrics, notably the McClellan Oscillator, have slipped below zero, further confirming bearish pressure. With multiple triggers occurring within a single month, analysts are treating this as a serious warning of a possible market top.

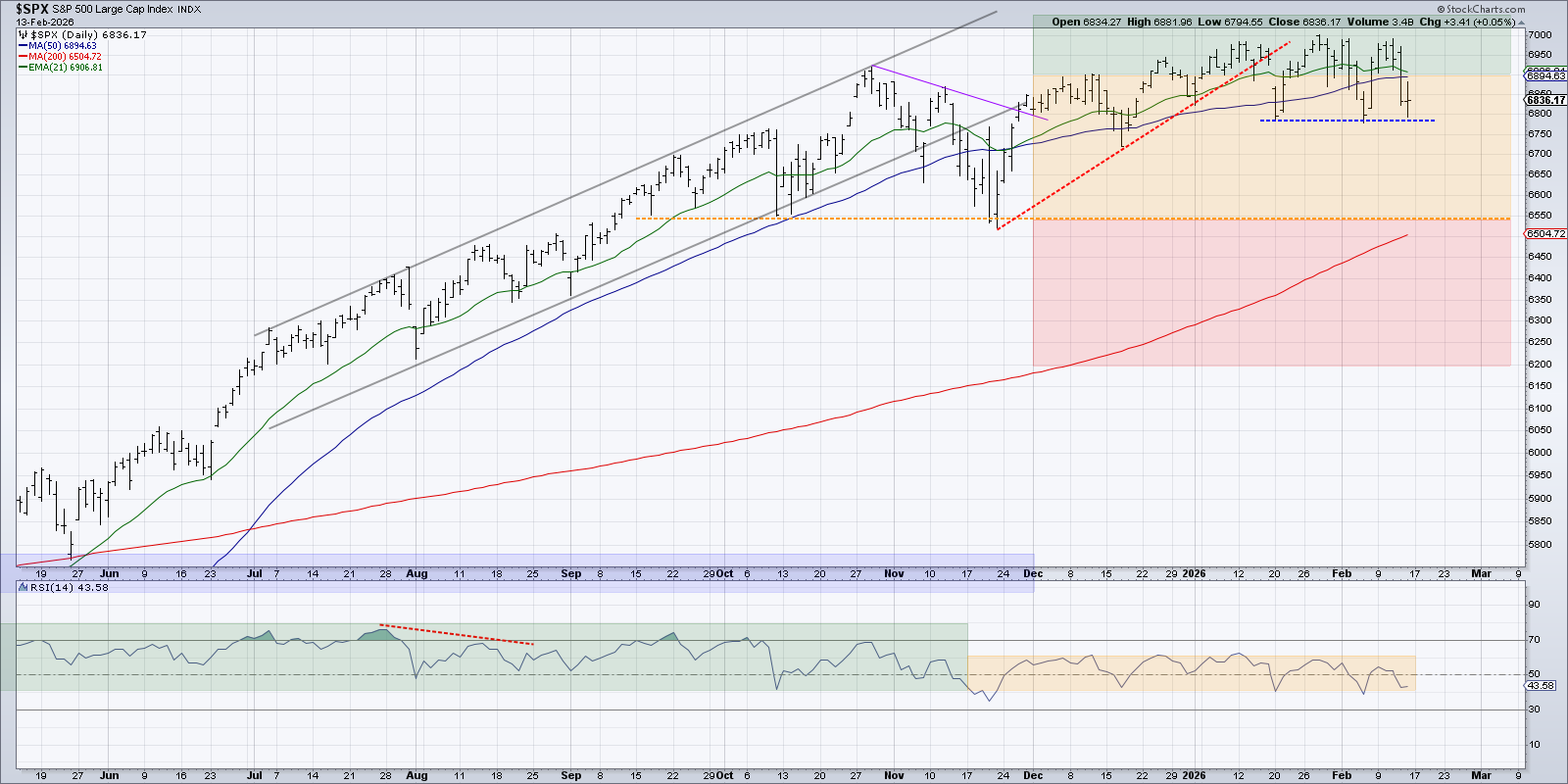

Technical View: S&P 500 Holds Neutral Stance

Even with the ominous signal, the S&P 500 is trading within a tight range — support near 6,800 and resistance just under 7,000. The Relative Strength Index (RSI) has hovered around the 50‑level since November, indicating a near‑even tug‑of‑war between bulls and bears.

Key tactical support sits around 6,800; a breach could expose the 6,550 level, which aligns with the 200‑day moving average and the lows recorded in October‑November. This confluence would be a clear signal of a deeper pullback.

Defensive Sectors Lead the Rotation

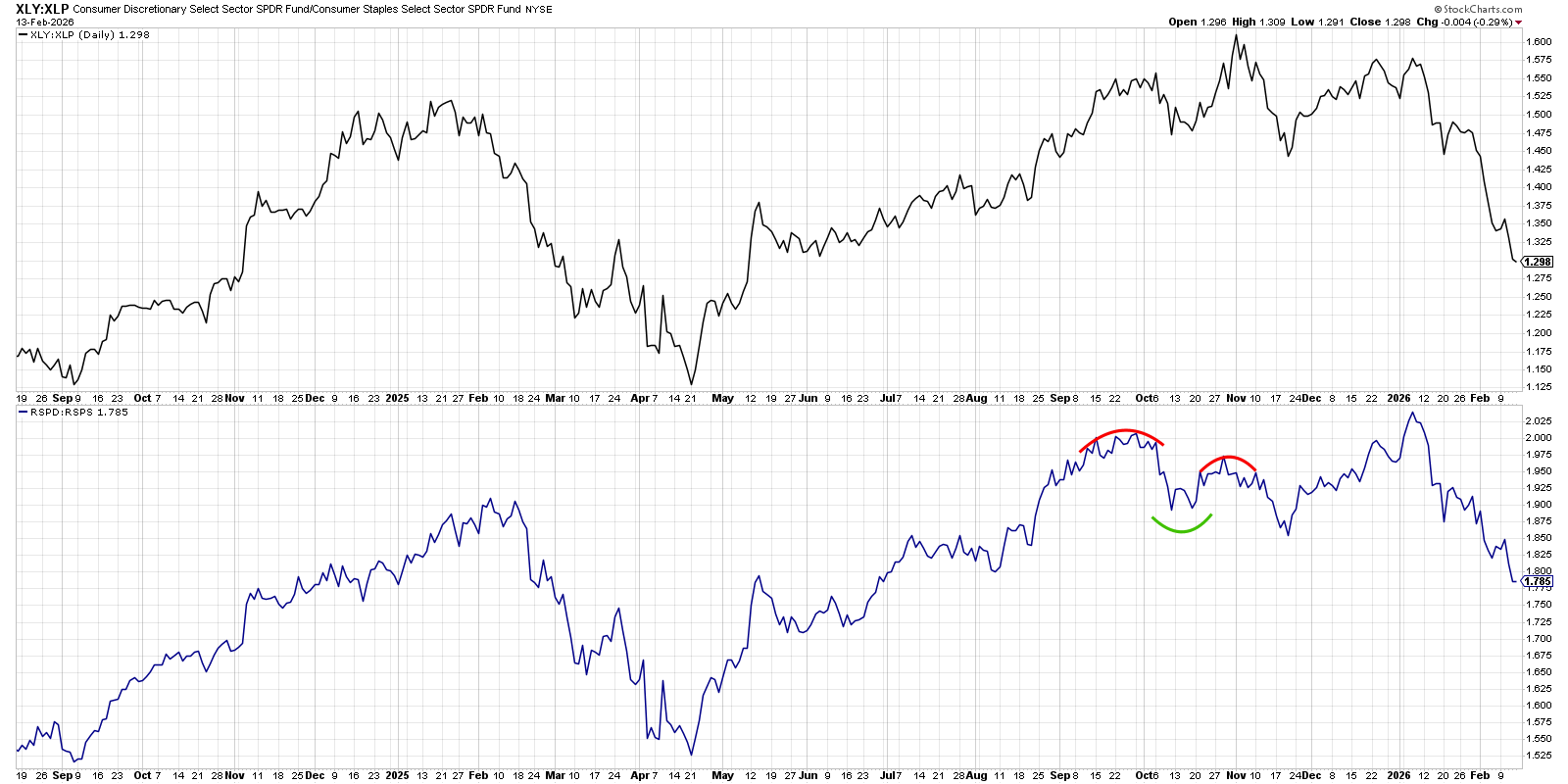

What validates the emerging defensive bias? The trio of Consumer Staples, Utilities and Real Estate have posted solid, double‑digit weekly gains, outpacing more aggressive sectors. This “offense vs. defense” dynamic underscores a risk‑off sentiment among investors.

Both cap‑weighted and equal‑weighted ratios of discretionary to staple exposure have slipped to three‑month lows, reinforcing the defensive tilt. Should the S&P 500 dip below its 6,800 foothold, the 6,550 zone becomes the next line in the sand.

In summary, while the broader market appears neutral, the confirmed Hindenburg Omen and the pronounced shift toward defensive and income‑generating sectors suggest caution. Traders and long‑term investors alike should monitor the 6,800‑6,550 support corridor for any decisive moves.

Source: Materials provided by https://articles.stockcharts.com.Note: Content may be edited for style and length.